Description

What This Service Is

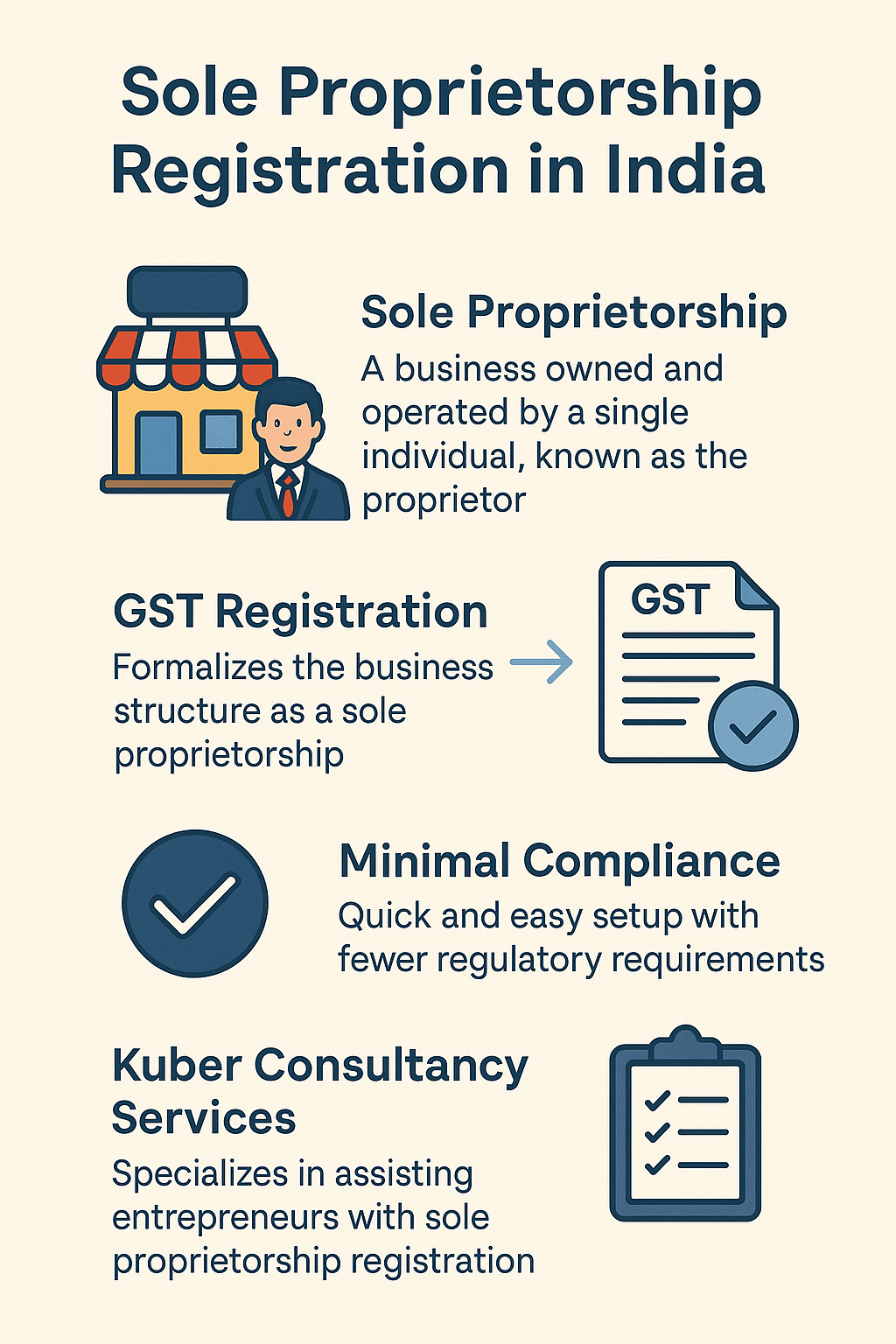

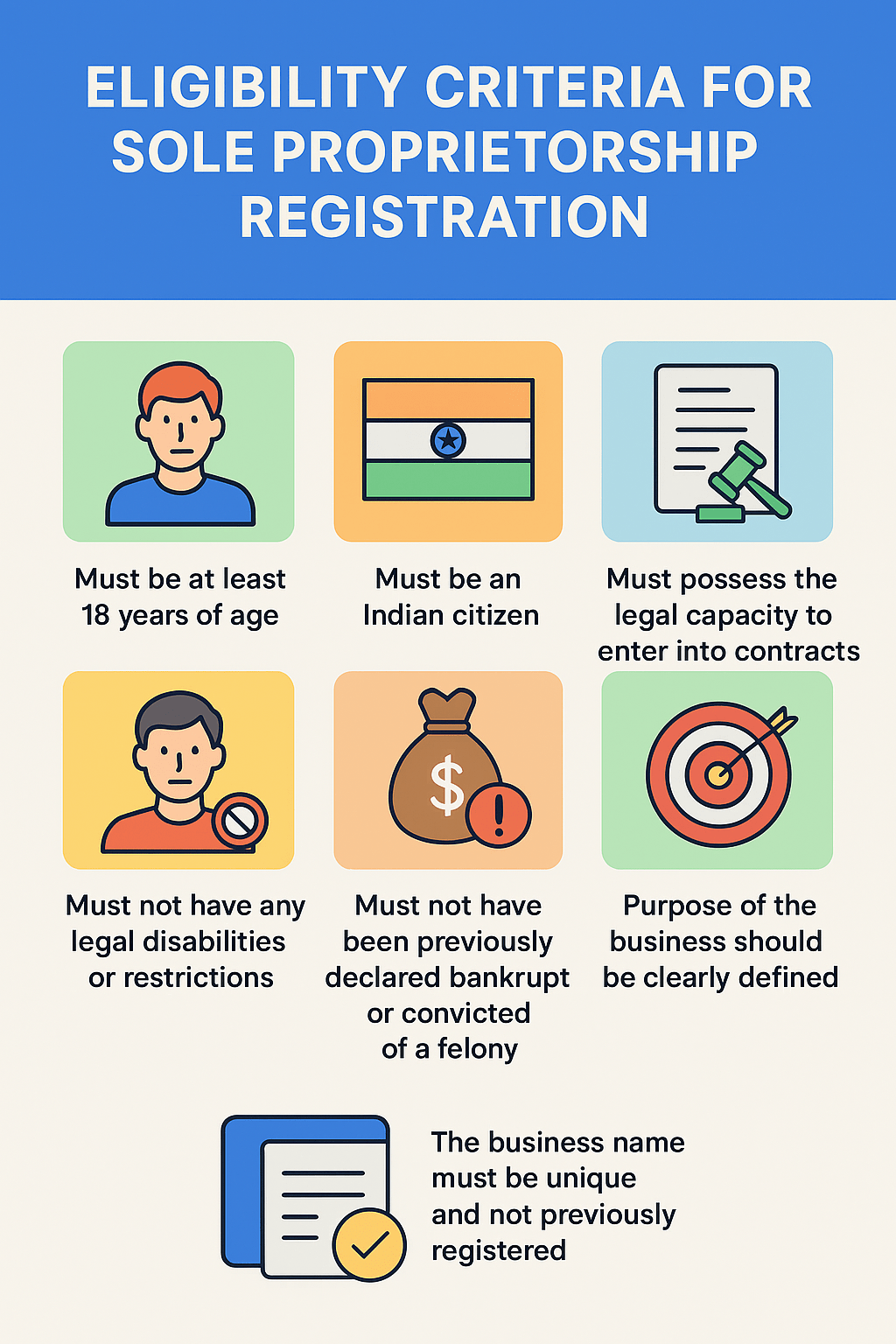

A Sole Proprietorship is one of the simplest forms of business structure in India, owned and managed by a single individual. In this structure, the proprietor and the business are legally the same entity.

This service provides professional assistance for setting up a Sole Proprietorship business in India by obtaining the required statutory and tax registrations applicable to the nature of business.

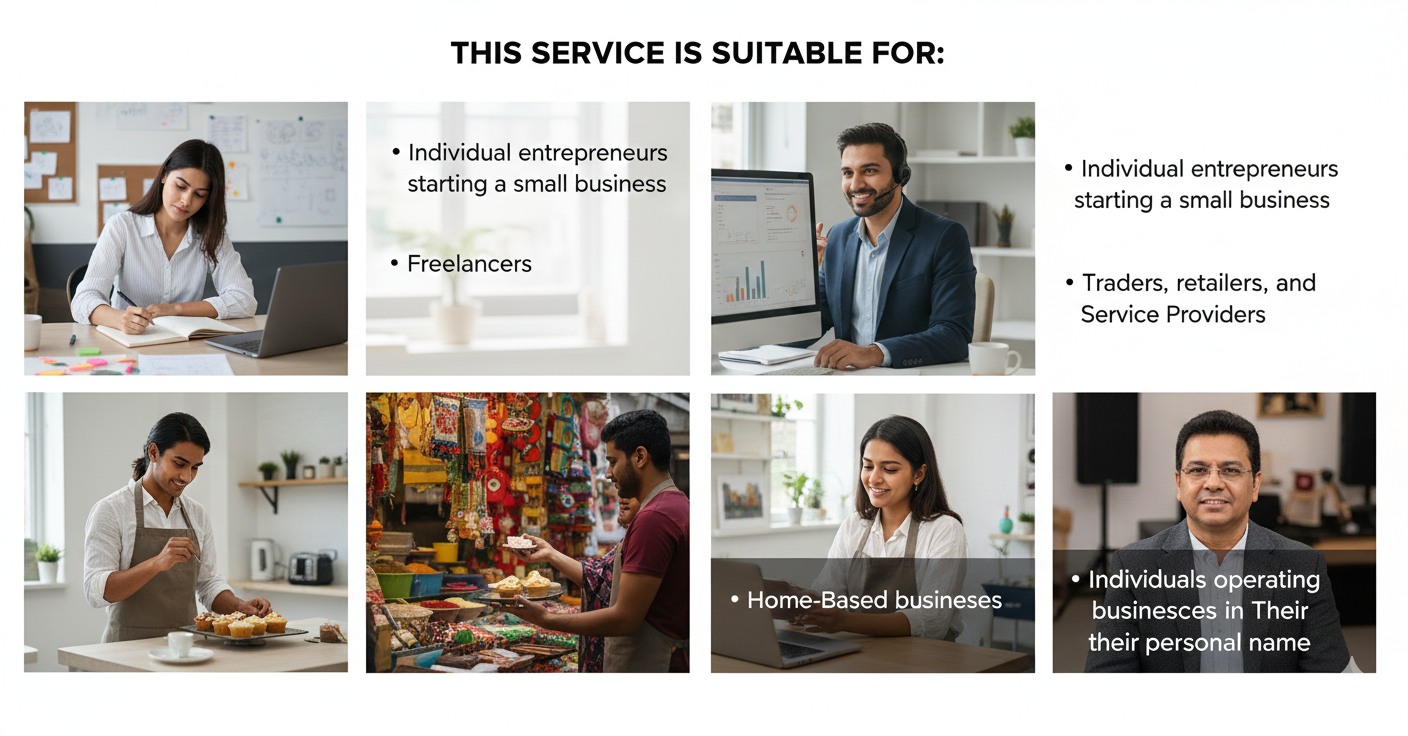

Who Should Opt for This Service

This service is suitable for:

• Individual entrepreneurs starting a small business

• Freelancers and consultants

• Traders, retailers, and service providers

• Home-based businesses

• Individuals operating businesses in their own name or trade name

Scope of Service (What We Will Do)

Under this service package, we assist with:

• Consultation on suitability of sole proprietorship structure

• Registration through applicable government registrations such as GST, MSME (Udyam), or Shop & Establishment, as applicable

• Documentation guidance and verification

• Support in obtaining basic registrations required to operate the business

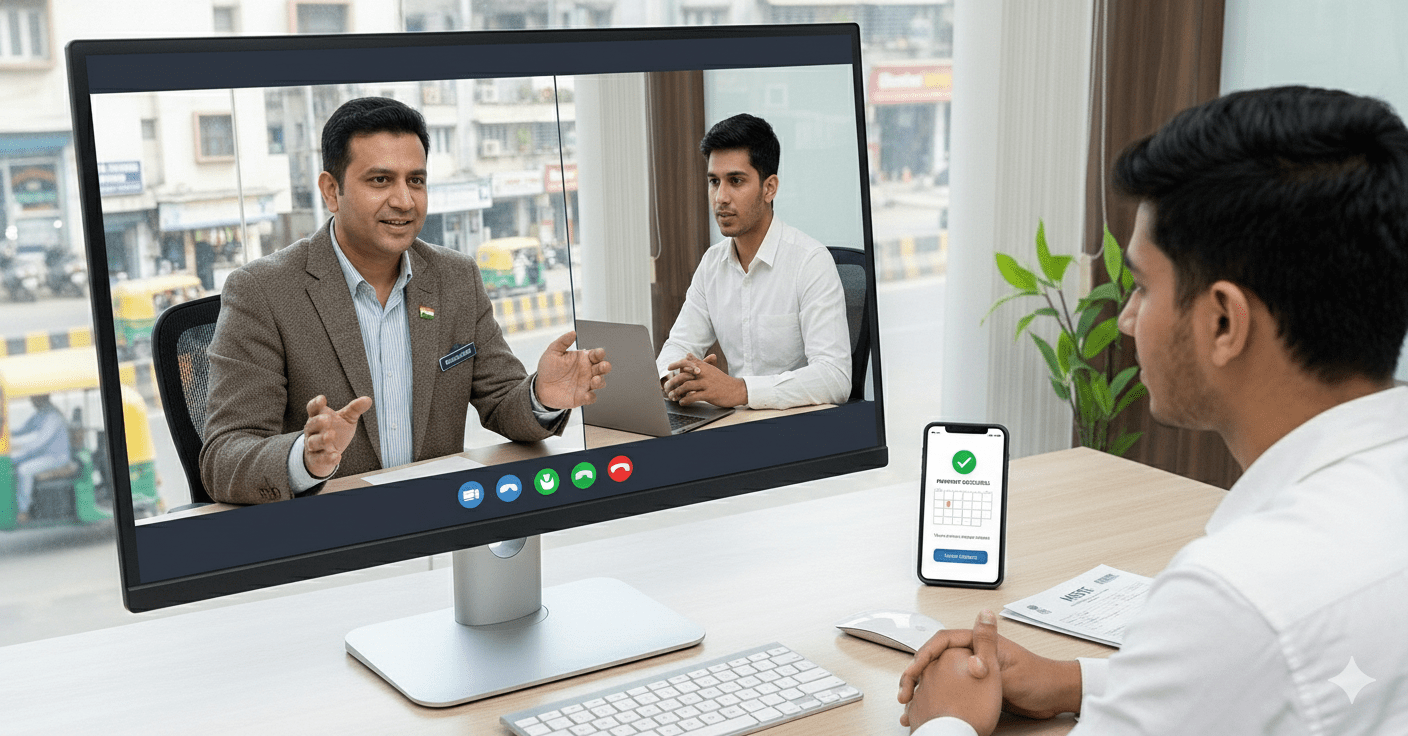

How the Service Is Delivered

This is a professional consultancy service delivered digitally.

After successful payment:

A Dedicated Business Manager is assigned

Documents are collected through the secure portal

Consultation and clarifications are handled online

Status updates are provided through the dashboard

No physical visit or paperwork exchange is required.

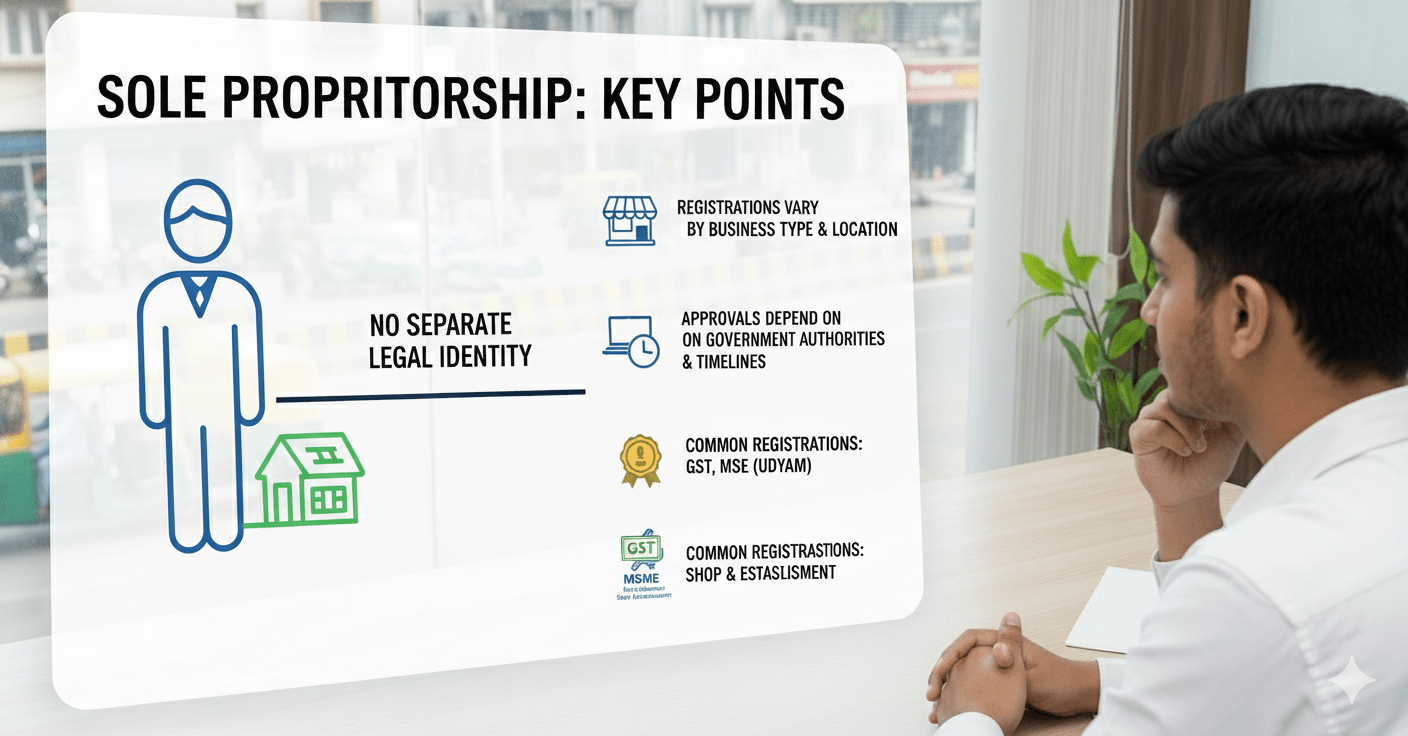

Important Notes & Legal Clarification

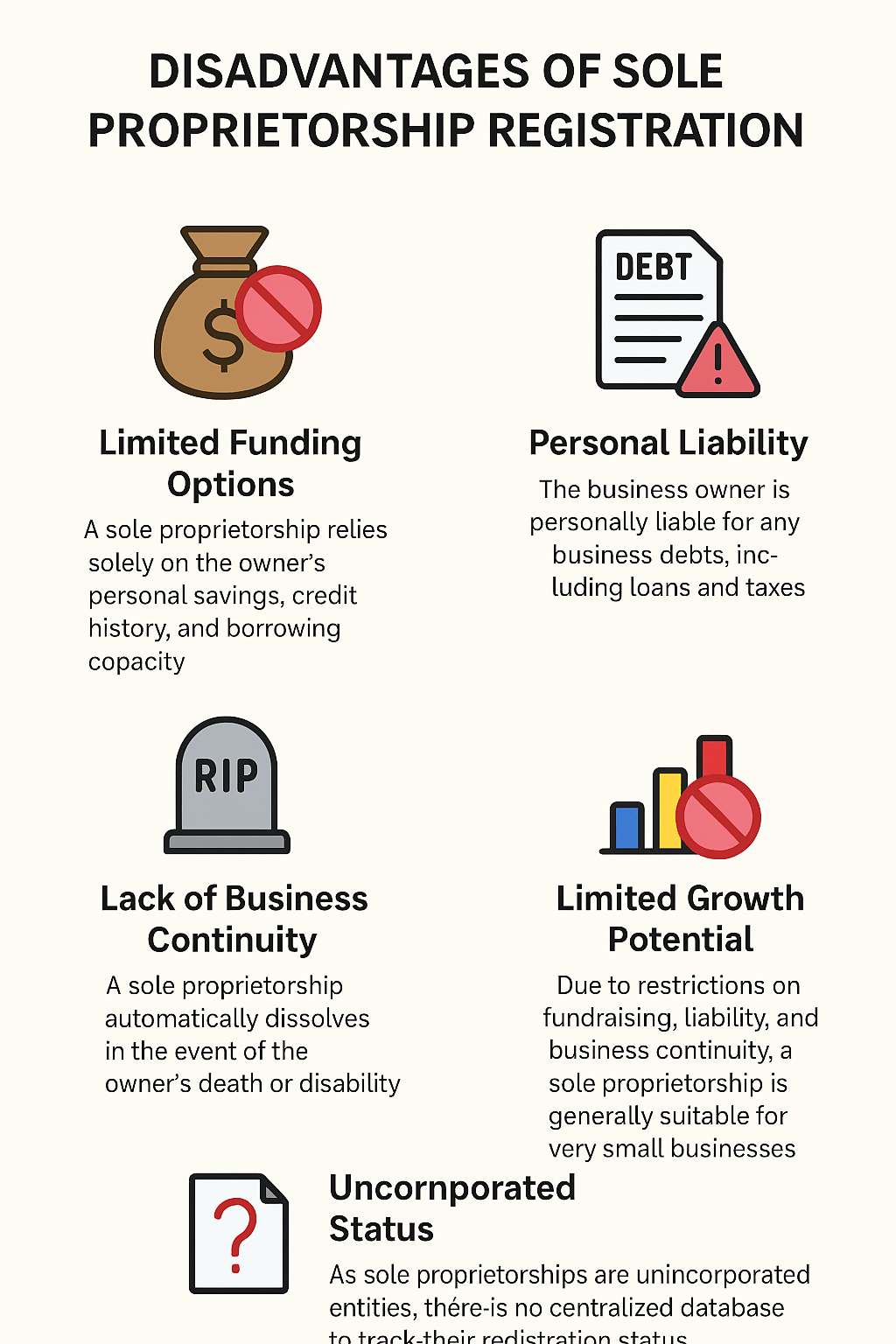

A Sole Proprietorship does not have a separate legal identity

The proprietor has unlimited personal liability

Registrations depend on business activity, location, and applicable laws

Approval timelines are governed by the respective departments

Nature of Service

This service package is listed as a virtual product only for online booking and payment purposes.

No physical goods are supplied or delivered.

Overall, I had a good experience with Kuber Consultancy Services for my Sole Proprietorship registration. The process was handled professionally and completed on time. There were a few minor delays in communication, but the team was supportive and resolved my queries properly.

Satisfied with the service and would recommend them to others.